Over 50 years of successful accounting partnerships.

We are a full service accounting firm dedicated to our clients, providing quality service with a quality team to assist your company with long term growth and stability.

Why UsHow can we help?

We offer a wide variety of services. If you aren’t seeing what you need here, please click the button to see everything we have to offer!

All Services

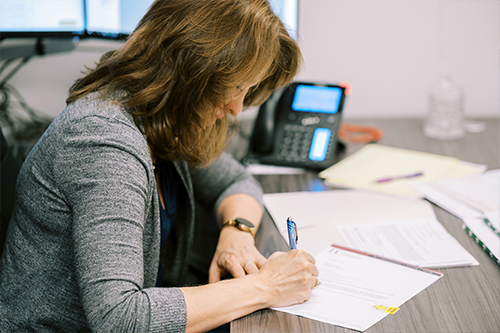

We have experience in many industries

Not your average team

With expertise across a number of industries and a number of disciplines, our team is able to help you with all of your accounting needs.

What have we been up to?

Navigating Education-Related Tax Benefits and Savings Strategies

~ Author – Sam Painter, Deluzio & Company Staff Accountant I~ Each year, a multitude of individuals embark on their college journeys, whether straight out of high school or later …

Read More

Alternative Fuel Vehicle Refueling Property Credit

~ Author – Dylan Lapham, Deluzio & Company Staff Accountant I~ Already own an electric vehicle or thinking about purchasing one? Installing an at home charging station? The Alternative Fuel Vehicle …

Read More

Avoiding Scammers

~ Author – Sam Painter, Deluzio & Company Staff Accountant I~ Post COVID there has been an increase in computer fraud and phishing attempts. This increase could be due to …

Read More